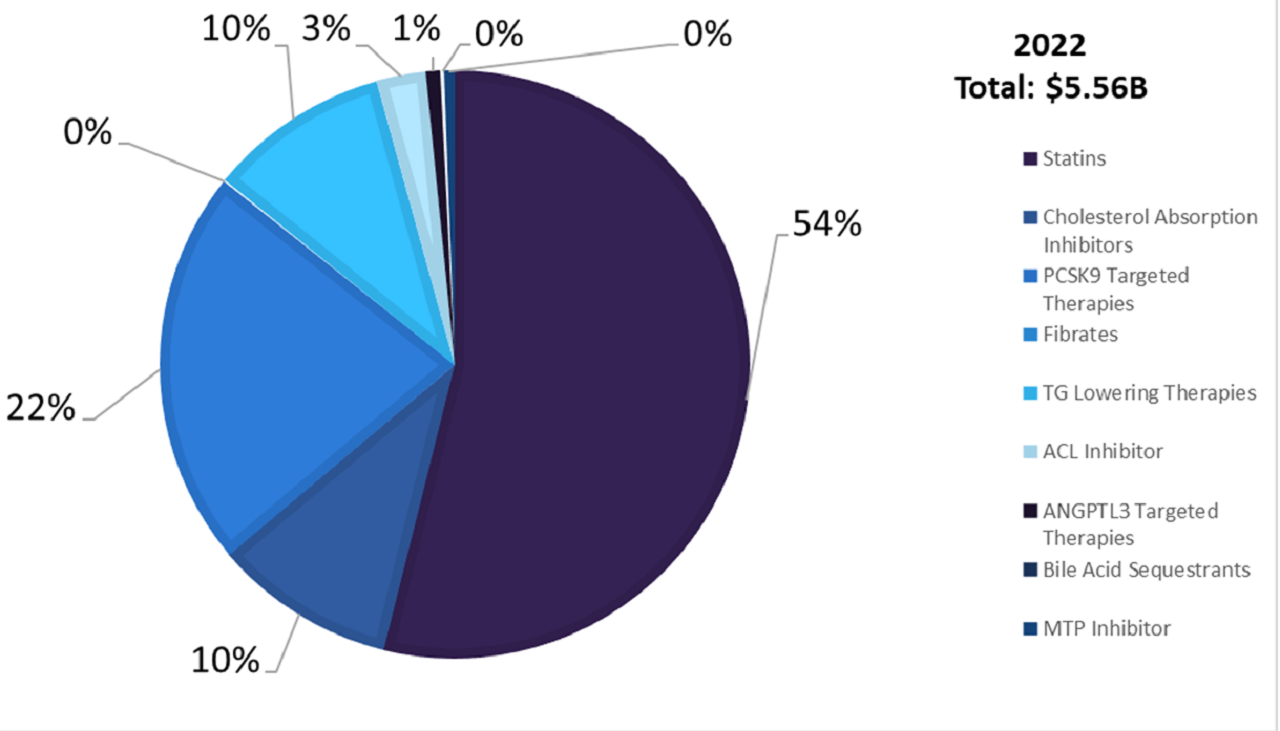

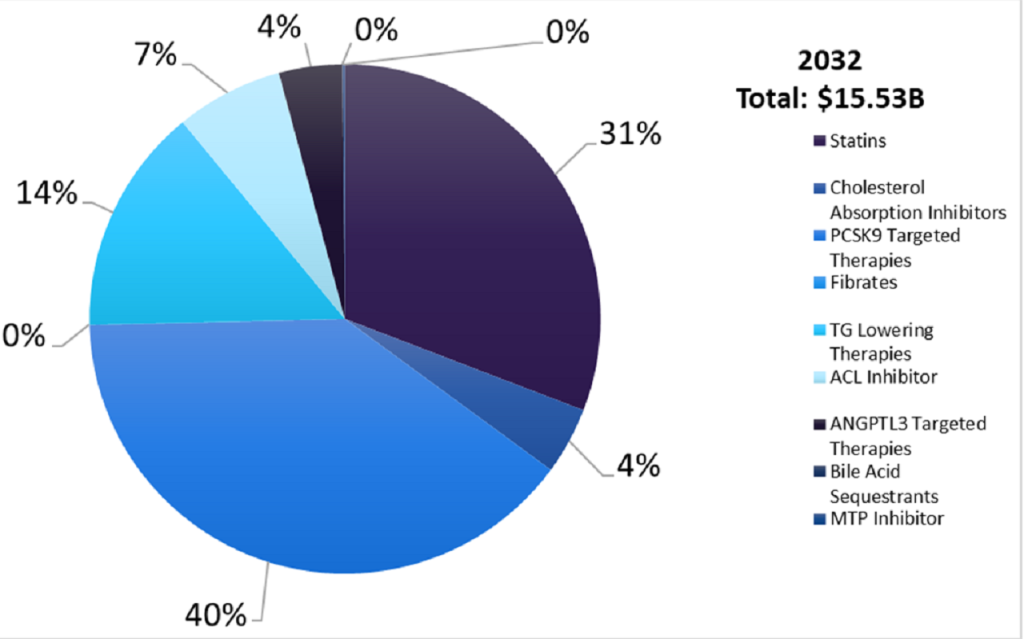

The dyslipidemia market is expected to grow from $5.56bn in 2022 to $15.53bn in 2032, at a compound annual growth rate of 10.8% across the seven major markets (7MM: US, France, Germany, Italy, Spain, UK, and Japan), according to GlobalData’s upcoming report, Dyslipidemia: Seven Market Drug Forecast and Market Analysis.

This growth during the forecast period is primarily due to the increasing global prevalence of dyslipidemia due to an increase in obesity, sedentary lifestyles, and unhealthy dietary habits. As the global population continues to age, the prevalence of dyslipidemia is likely to increase.

Additionally, improved awareness about the health risks associated with dyslipidemia and increased efforts in screening and diagnosis are expected to lead to more people being diagnosed with the condition. Moreover, global sales will increase due to the launch of several late-stage pipeline therapies.

GlobalData forecasts that NewAmsterdam Pharma’s cholesteryl ester transfer protein (CETP) inhibitor, obicetrapib, will be the most promising pipeline therapy for the condition. Other promising pipeline therapies include Merck’s first oral proprotein convertase subtilisin/kexin type 9 (PCSK9) inhibitor, MK-0616, and Akcea Therapeutics’ apoC-III antisense RNAi oligonucleotide, olezarsen.

The continued generic erosion of Pfizer’s Lipitor, AstraZeneca’s Crestor (rosuvastatin), as well as Merck’s Zetia (ezetimibe) across the 7MM will lead to a decrease in sales of statins and cholesterol absorption inhibitors, while the high cost and increased use of PCSK9 inhibitors will be a driver of 7MM sales throughout the forecast period.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Of the 7MM included in this forecast, the US is the most significant contributor to the dyslipidemia market size, accounting for 74% of sales in 2022 and 78% of estimated sales in 2032.

The dominant role of the US is primarily due to the higher price tag of US therapeutics as compared with the other markets, and the higher prevalence of dyslipidemia. Spain is predicted to contribute the least to dyslipidemia drug sales: only 3% in 2022 and 2% in 2032.

The figures below summarise the projected growth in the dyslipidemia market across the 7MM from 2022 to 2032.

Major drivers of the dyslipidemia market growth during the forecast period are:

- The increasing global prevalence of dyslipidemia due to an increase in obesity, sedentary lifestyles, and unhealthy dietary habits. As the global population continues to age, the prevalence of dyslipidemia is likely to increase.

- Improved awareness about the health risks associated with dyslipidemia and increased efforts in screening and diagnosis are expected to lead to more people being diagnosed with the condition.

- Therapies with new targets will enter the market, which will significantly boost market growth.

- The launch of the first oral PCSK9 inhibitor, Merck’s MK-0616, as well as other promising pipeline therapies, including NewAmsterdam’s oral CETP inhibitor, obicetrapib, and Akcea Therapeutics’s apoC-III, olezarsen.

Major barriers that will restrict the growth of the dyslipidemia market during the forecast period are:

- The price of novel launched drugs for dyslipidemia and the restriction of access to highly priced new therapies.

- Widespread use of cheap, generic drugs making it difficult for high-priced branded therapies to penetrate the market.

- Continued generic erosion of Pfizer’s Lipitor, AstraZeneca’s Crestor, as well as Merck’s Zetia across the 7MM.