Early stage biotech companies (biotechs) rely heavily on external funding to advance their research and development (R&D) programs. Robust fundraising strategies are critical for advancing discoveries within the biopharma industry’s highly cost-intensive R&D environment, where early-stage biotechs operate with high stakes. In 2025, however, the landscape for these funding-dependent companies remains challenging, with GlobalData recently reporting a 5% contraction in year-on-year deal value during the first four months of 2025, mostly driven by a decline in mergers and acquisitions (M&A).[i]

“The current financial market is tough, and biotechs are finding it very difficult to get access to capital,” comments Samir Kagrana, Global Head of Strategic Deals at Fortrea, a contract research organisation (CRO). “It takes at least ten years to develop a molecule, and that development is becoming more and more complex and expensive over time.”

“Many biotechs are struggling to realise the full potential of the intellectual properties that they have, which not only impacts the biotech’s survival but also the industry as a whole. Even if they do secure funds, they may not have enough for the parallel development of multiple assets, so they need to prioritise the most promising one out of three or four potential therapies.”

In 2025, limited access to capital is forcing these companies to make difficult strategic decisions, potentially delaying or halting the development of groundbreaking therapies that could benefit patients and advance the field. So, how did we get to this point?

The aftermath of the biotech boom

In 2021, favourable economic conditions, significant investor optimism, and heightened attention during the COVID-19 pandemic response led to record-high levels of deal volume and value in the industry, marking a breakthrough year for many emerging biotechs and start-ups.

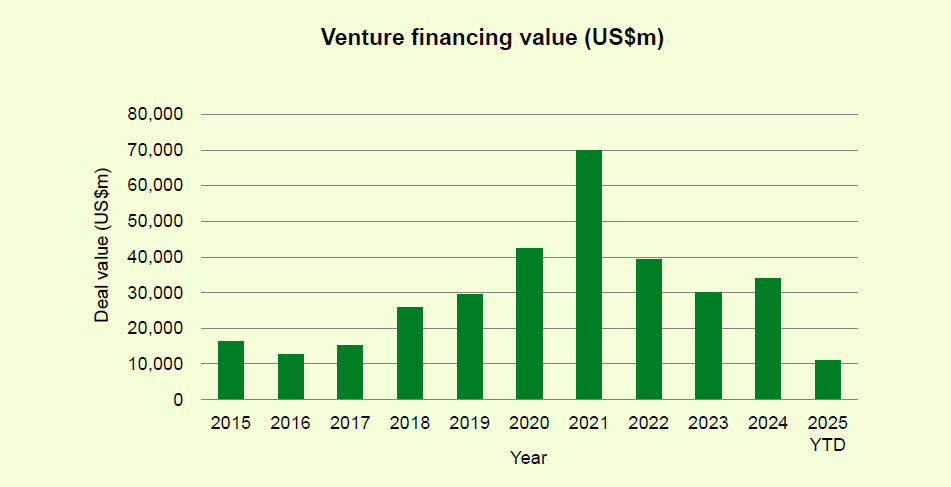

According to GlobalData’s Deals database, the value of all pharmaceutical venture capital (VC) deals reached almost $70 billion in 2021. As the chart below shows, this was a considerable leap from previous years, making the sharp decline seen in 2022 and 2023 somewhat unsurprising.

When venture financing boomed in 2021, many biotechs subsequently rushed to the public markets. Initial public offering (IPO) numbers soared in the industry and then plummeted soon after. Experts believe many companies went public with inflated valuations, contributing to a more cautious investment environment in the following years. This was compounded by high interest rates and inflation, forcing many start-ups to delay their IPOs until market conditions improved.

Venture financing is now recovering. According to GlobalData, the value of all VC arrangements in the industry increased by almost 15% from the previous year, putting it at $34 billion – higher than pre-pandemic figures.

Biopharma IPOs also saw an upturn last year, with 50 completed IPOs raising a total of $8.52 billion. This represented a 68% increase from the amount raised in 2023.[ii] In particular, analysts at GlobalData noted a recent trend towards high-value IPOs involving more established companies. This has left early-stage firms in a difficult position.

Alison Labya, Business Fundamentals Analyst at GlobalData, explains: “Despite the overall increase in IPO value raised, discovery and preclinical-stage companies saw a four-fold drop in total IPO value from $490.6 million in 2023 to $112.5 million in 2024, indicating a shift in public investor preference towards more advanced stage companies.”

Fortunately, optimism levels are improving amongst the industry. In a survey run by GlobalData in late 2023, 44% of the industry was optimistic about a recovery of biotech funding. In the same survey run one year later, this increased to 50%.[iii]

The importance of a compelling value proposition

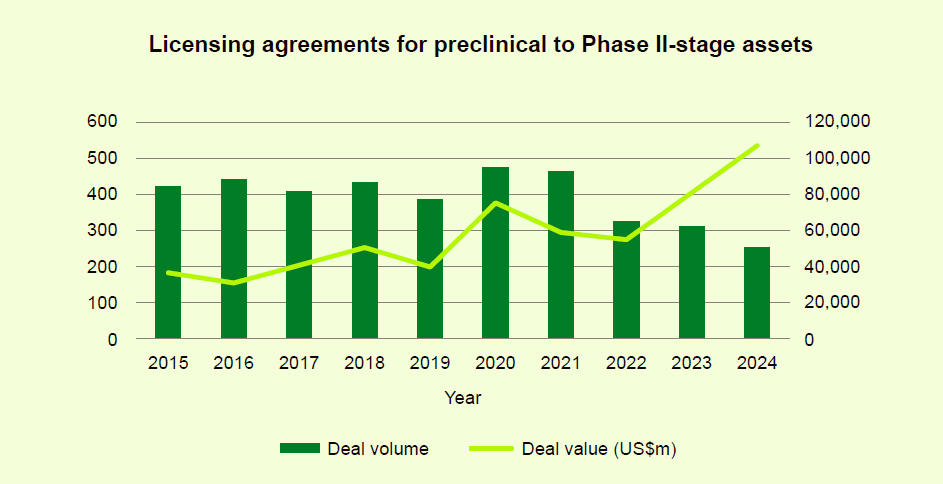

The upshot is that investors are now being more selective – a trend that is mirrored amongst industry partnerships as well. Pharmaceutical companies spent $108 billion on licensing agreements in 2024 – by far the highest amount across the past decade – but these funds were distributed across fewer deals than normal. The average number of licensing agreement deals between 2015 and 2020 was 429, while 2023 saw 308 deals, followed by 257 in 2024. This means that while pharma is spending more on acquiring biotech assets, fewer acquisitions are being made overall. Essentially, the stakes are higher than ever for biotech success.

In this cautious investment climate, strong and compelling value propositions are essential for persuading investors and potential licensing partners to take risks on new opportunities rather than prioritising the existings. At the same time, emerging biotechs need a well-crafted strategy for prioritising their assets, navigating investment opportunities, and finetuning their commercial positioning.

Collaborations with other companies can help along this process. However, with limited funds for engaging various service providers, biotechs should team up with a development partner that can assist in all these aspects in addition to clinical development, regulatory strategy, and future market access. This is where CROs come in, providing an end-to-end service to help biotechs with limited internal resources gain access to the expertise and experience needed to navigate clinical development, asset prioritisation, funding opportunities, and regulatory pathways with significantly higher chances of success.

To learn more about evolving market dynamics in the biotech landscape and the importance of CRO partnerships, please download the whitepaper below.

[i] https://www.globaldata.com/media/business-fundamentals/cautious-investor-sentiment-pulls-global-deal-activity-down-5-yoy-in-first-four-months-of-2025-finds-globaldata/

[ii] https://www.globaldata.com/media/business-fundamentals/biotech-ipos-surge-68-4-yoy-to-8-52-billion-in-2024-amid-public-market-recovery-reveals-globaldata/

[iii] GlobalData, Thematic Intelligence: The State of the Biopharmaceutical Industry, 2024 and 2025 editions